an art

a process

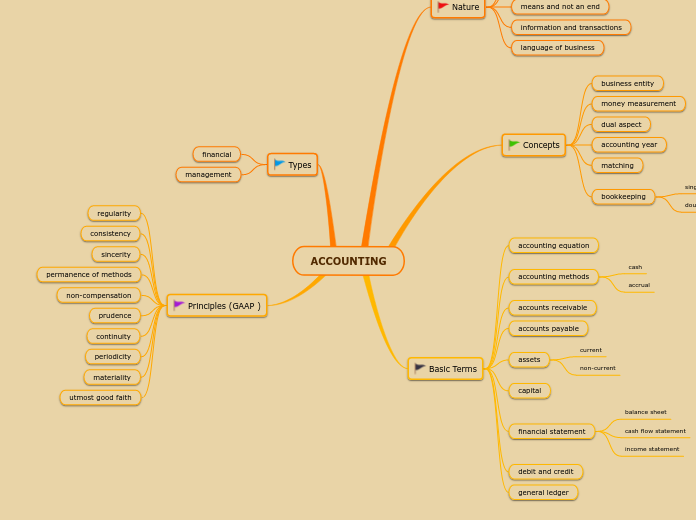

means and not an end

information and transactions

language of business

business entity

money measurement

dual aspect

accounting year

matching

bookkeeping

single-entry

double-entry

accounting equation

accounting methods

cash

accrual

accounts receivable

accounts payable

assets

current

non-current

capital

financial statement

balance sheet

cash flow statement

income statement

debit and credit

general ledger

financial

management

regularity

consistency

sincerity

permanence of methods

non-compensation

prudence

continuity

periodicity

materiality

utmost good faith